Business Owners & SMEs: What Budget 2026-27 Could Change

The Business Owner’s Budget

For Pakistan’s business owners, SMEs and traders, Budget 2026-27 arrives at a difficult moment. Inflation is still elevated, margins are compressed, and the IMF’s fiscal consolidation demands more revenue from the formal sector — not less.

The Finance Ministry must increase tax collection while keeping the business community onside. That tension defines everything in Budget 2026-27 for the commercial sector.

This post covers the four key areas every business owner must watch on June 5.

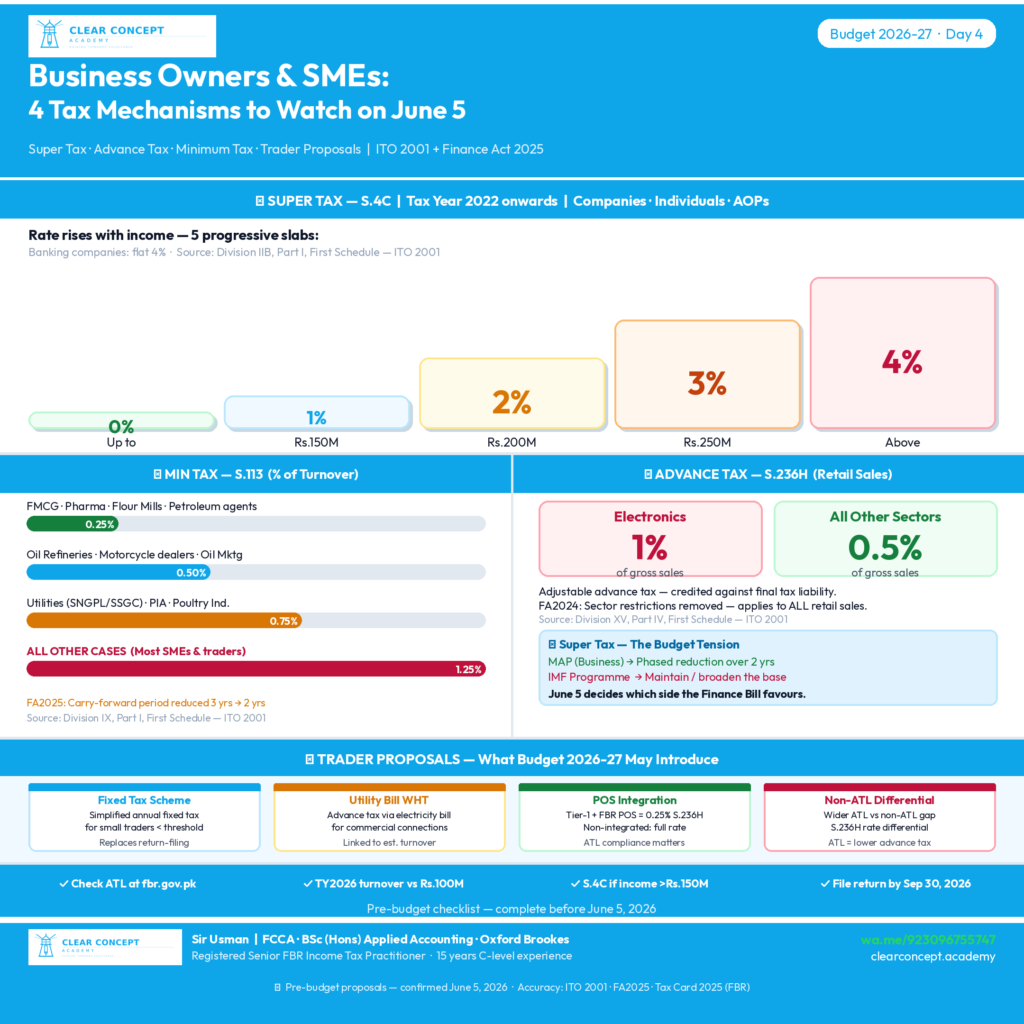

1. Super Tax — Section 4C

What the Law Currently Says

Under Section 4C, Income Tax Ordinance 2001 (inserted by Finance Act 2022), a super tax is imposed on high-earning persons for Tax Year 2022 and onwards.

The tax applies to income as defined under S.4C(2), which includes:

- Profit on debt, dividends, capital gains, brokerage and commission

- Taxable income under S.9 (excluding brought-forward losses and depreciation)

- Imputable income as defined in S.2(28A)

- Income computed under the Fourth, Fifth, Seventh and Eighth Schedules

Current rates (Division IIB, Part I, First Schedule):

| Income Threshold | Super Tax Rate |

|---|---|

| Up to Rs.150 million | 0% |

| Rs.150M – Rs.200M | 1% |

| Rs.200M – Rs.250M | 2% |

| Rs.250M – Rs.300M | 3% |

| Above Rs.300 million | 4% |

| Banking companies | 4% |

The super tax is payable in advance under S.147 and collected/deposited per S.137.

What Budget 2026-27 May Change

The government has faced consistent pressure from the business community to reduce or phase out the super tax, arguing it discourages reinvestment and penalises growth. Simultaneously, the IMF’s fiscal targets require the government to maintain or expand revenue from direct taxes.

Possible proposals being discussed:

- Rate increase on the Rs.300M+ bracket (from 4% to 5% or higher)

- Extension to lower income brackets — bringing businesses earning Rs.100M+ into the net

- Status quo — no change to current structure

The Finance Act 2025 explanation confirmed that the super tax exemption applies to capital gains on disposal of a specified personal-use residential property (held 15+ years and declared in wealth statement), but this is a narrow carve-out.

What to watch on June 5: Any amendment to Division IIB of Part I of the First Schedule.

2. Advance Tax on Sales to Retailers — Section 236H

What the Law Currently Says

Under Section 236H, ITO 2001 (added by Finance Act 2013, substantially amended by Finance Act 2024), every manufacturer, distributor, dealer, wholesaler or commercial importer, at the time of sale to retailers, must collect advance tax at rates specified in Division XV of Part IV of the First Schedule.

Current rates (Division XV):

| Category of Sale | Rate of Tax |

|---|---|

| Electronics | 1% of gross amount of sales |

| All other categories | 0.5% of gross amount of sales |

This is an adjustable advance tax — credit is allowed against the retailer’s final tax liability for the tax year in which it was collected.

Note: The Finance Act 2024 removed the sector-specific restriction that previously limited S.236H to named sectors (pharmaceuticals, poultry, edible oil, electronics, sugar, cement, etc.). As of Finance Act 2024, it applies broadly to all retail sales.

What Budget 2026-27 May Change

Advance tax on retailers is a key compliance tool — and a recurring target for upward revision. With the government pushing for broader retail sector documentation, proposals include:

- Rate increase for non-ATL retailers — raising the 0.5% general rate for non-filers

- Sector-specific additions — bringing new product categories into the 1% bracket

- Compliance linkage — conditions tying S.236H rates to real-time POS integration

What to watch on June 5: Any amendment to Division XV of Part IV of the First Schedule.

3. Minimum Tax on Turnover — Section 113

What the Law Currently Says

Section 113, ITO 2001 imposes a minimum tax on the income of certain persons. It applies where, for any reason allowed under the Ordinance (losses, exemptions, credits, allowances), a person pays no tax or pays tax below the minimum rate.

It applies to:

- Resident companies

- Permanent establishments of non-resident companies

- Individuals with annual turnover of Rs.100 million or above (Tax Year 2017 onwards)

- Associations of Persons with annual turnover of Rs.100 million or above

Current minimum tax rates (Division IX, Part I, First Schedule):

| Person / Category | Minimum Tax Rate (% of turnover) |

|---|---|

| Oil refineries, motorcycle dealers, oil marketing companies | 0.5% |

| Distributors of pharmaceuticals, FMCG, cigarettes; petroleum agents; rice mills; flour mills; Tier-1 integrated retailers; e-commerce persons; used vehicle dealers | 0.25% |

| Poultry industry, SNGPL/SSGC (turnover >Rs.1B), PIA | 0.75% |

| All other cases | 1.25% |

Finance Act 2025 change — carry-forward period reduced:

Prior to Finance Act 2025, minimum tax paid in excess of actual liability could be carried forward for three succeeding tax years. Finance Act 2025 reduced this to two years. This means businesses that regularly pay minimum tax have a shorter window to offset it against future profitable years.

What Budget 2026-27 May Change

The general rate of 1.25% applies to the majority of SMEs and trading businesses not in the named categories above. Proposed changes include:

- Rate increase — raising the general 1.25% rate to 1.5% or 2% for certain businesses

- Turnover threshold reduction — bringing individuals and AOPs below the Rs.100 million threshold into minimum tax

- Sector expansion — adding new categories at different rate tiers

What to watch on June 5: Any amendment to Division IX of Part I of the First Schedule, or to the S.113 threshold provision.

4. Trader Proposals — The Retail & Wholesale Sector

Background: The Trader Tax Standoff

Pakistan’s retail and wholesale trade sector — the vast majority of which operates informally — has been a persistent friction point between FBR and the business community. Previous attempts to impose fixed-tax or turnover-based schemes on traders have met with street-level resistance and political rollbacks.

Budget 2026-27 is expected to revive this effort under IMF pressure to document the retail economy.

What Is Being Proposed

Fixed Tax Scheme for Small Traders:

A simplified fixed annual tax for small traders below a defined turnover threshold — similar in concept to the earlier “Easy Tax” schemes. The amount would vary by trade category, business size and location. This would replace normal return-filing obligations for qualifying traders.

Advance Tax Linkage to Utility Connections:

Proposals to collect advance tax at source from traders through electricity bills — linking commercial connection consumption to estimated business turnover. This has been discussed since 2023 and resurfaces every budget season.

POS Integration Incentives/Penalties:

Continued push to integrate Tier-1 retailers with FBR’s real-time POS system. Integrated retailers benefit from reduced S.236H rates (0.25%); non-integrated retailers face standard rates.

S.236H non-filer differential:

The current structure already has a non-filer penalty built into S.236H via ATL status — but proposals to widen this gap further are on the table.

What to Watch on June 5

- Any new simplified tax scheme for traders (look for new section or Part in the Finance Bill)

- Amendments to S.236H rates — especially for non-ATL traders

- Advance tax collection mechanism via utilities or banking channels

- New compliance conditions for wholesale-to-retail supply chains

Summary: 4 Things Business Owners Must Watch June 5

| Section | Current Position | Risk |

|---|---|---|

| S.4C Super Tax | 0%–4% on income Rs.150M+ | Rate increase for Rs.300M+ bracket |

| S.236H Advance Tax | 0.5%–1% on retail sales | Rate hike for non-filers / non-ATL |

| S.113 Minimum Tax | 1.25% general rate on turnover | Rate increase / threshold reduction |

| Trader Regime | No fixed scheme currently | New simplified tax scheme possible |

What SMEs and Business Owners Must Do Now

Before June 5:

• Confirm your ATL (Active Taxpayer List) status at fbr.gov.pk

• Estimate your Tax Year 2026 turnover — know if you’re above the Rs.100M minimum tax threshold

• Calculate your current S.4C exposure if your income exceeds Rs.150 million

• Ensure any retail purchases are from registered, ATL-enrolled suppliers to minimise your S.236H burden

After June 5:

• Read the Finance Bill 2026-27 — specifically Division IIB, Division IX and Division XV of the First Schedule

• Recalculate your advance tax instalments under S.147 if super tax rates change

• Consult your tax advisor before making any major commercial decisions based on budget announcements

The Broader Context

Pakistan’s tax-to-GDP ratio remains one of the lowest in the region. The IMF’s Extended Fund Facility targets a meaningful increase in revenue collection as a share of GDP over the next three years. This means the formal business sector — manufacturers, distributors, wholesalers and larger retailers — will face continued pressure through advance tax, minimum tax and super tax mechanisms.

The budget will not reduce this burden. The question is how it is structured — and whether the government accompanies increased tax demands with genuine administrative simplification for compliant businesses.

Budget 2026-27 drops June 5, 2026. ClearConcept Academy will publish a full analysis within hours of the announcement.

📅 Budget 2026-27 Series — All Posts

- Day 1 — Salaried Class: Income Tax Relief Proposals

- Day 2 — Property Investors & Real Estate: Tax Changes

- Day 3 — Freelancers & IT Sector: Exemptions & Tax

- Day 4 — Business Owners & SMEs: Super Tax, Min Tax & Trader Proposals (this post)

About This Analysis

All legal references in this article are verified against:

- Income Tax Ordinance 2001 (as amended)

- Finance Act 2025

- Finance Act 2025 Explanation (FBR)

- Tax Card 2025 (FBR)

⚠️ Pre-budget disclaimer: All proposals discussed above reflect pre-budget discussions and are subject to confirmation in the Finance Bill 2026-27, announced June 5, 2026.

Sir Usman | FCCA · BSc (Hons) Applied Accounting, Oxford Brookes | Registered Senior FBR Income Tax Practitioner | 15 years C-level industry experience

ClearConcept Academy — clearconcept.academy | WhatsApp: +92 309 6755747