# Will Budget 2026-27 Kill or Protect the IT Exemption?

Date: June 3, 2026

Category: Pakistan Taxation · Budget 2026-27 · IT Sector · Freelancers

Status: Pre-budget proposals only — final decision confirmed June 5, 2026

The Most Important Question for Pakistan’s Dollar Earners

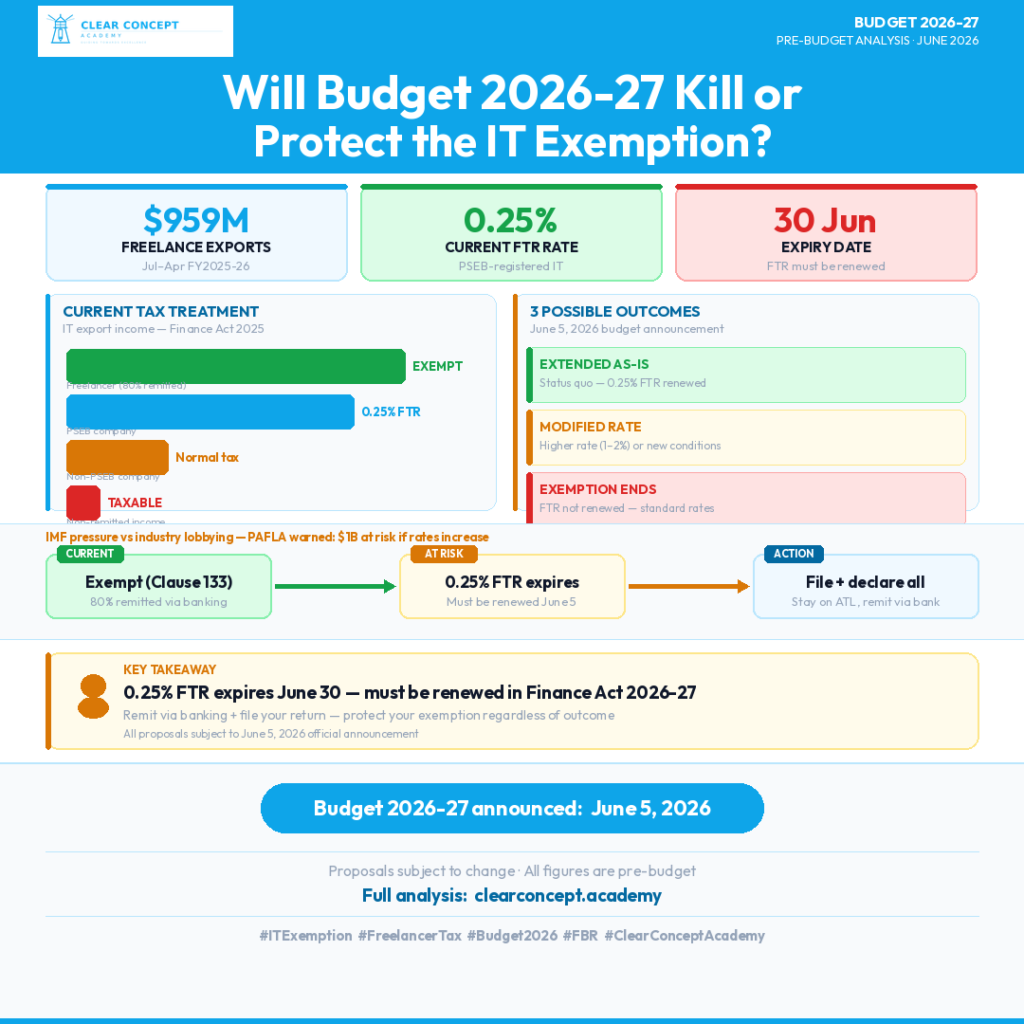

Pakistan’s freelancers and IT exporters are entering Budget 2026-27 with a single critical question: will the government extend the 0.25% Final Tax Regime for IT exports — or let it expire on June 30, 2026?

This is not a hypothetical. The current 0.25% tax rate is scheduled to expire. If the Finance Bill 2026-27 does not extend it, freelancers and IT exporters face a sudden jump in their effective tax rate.

The stakes are substantial. According to the State Bank of Pakistan, freelancing export earnings reached $959 million in the first ten months of FY2025-26 — up 49% from the same period last year. Pakistan is close to crossing the $1 billion threshold in freelancing income alone.

Budget 2026-27 will determine whether that growth continues — or reverses.

The Current Legal Framework — Finance Act 2025

Clause 133 — The Core Exemption

Under Clause 133, Part I, Second Schedule, Income Tax Ordinance 2001, income from exports of:

- Computer software

- IT services

- IT-enabled services (ITeS)

is exempt from income tax — subject to the condition that 80% of export proceeds are remitted to Pakistan through normal banking channels.

Persons claiming this exemption remain subject to minimum tax on turnover under Section 113 ITO 2001.

The 0.25% Final Tax Rate

For PSEB-registered entities (Pakistan Software Export Board), IT export proceeds qualify for a 0.25% Final Tax Regime (FTR) — a concessionary rate.

Critical fact: This 0.25% rate is scheduled to expire on June 30, 2026. It must be explicitly renewed in the Finance Act 2026-27.

Who Qualifies

| Category | Current Tax Treatment |

| Freelancer — individual, 80% remitted via banking | Exempt from tax (Clause 133) |

| PSEB-registered IT company | 0.25% FTR on export proceeds |

| Non-registered IT company | Standard corporate tax rates |

| Freelancer — income not remitted via banking | Taxable at normal slab rates |

What P@SHA Proposed — And Then Retracted

The Pakistan Software Houses Association (P@SHA) submitted a budget proposal recommending the closure of the 0.25% tax concession — arguing that the exemption benefits large IT exporters disproportionately and creates an unlevel playing field against domestic software companies.

The proposal triggered an immediate and forceful response from the freelancing community.

The Pakistan Freelancers Association (PAFLA) responded publicly, stating that Pakistan could lose $1 billion in freelancer earnings if income tax on freelancers is increased. PAFLA called the P@SHA proposal an attack on individual freelancers who have nothing to do with large corporate IT firms.

P@SHA subsequently retracted its proposal — confirming it had not intended to target individual freelancers.

The fact that the proposal was even floated signals the budget negotiations around this exemption were serious.

The IMF Factor

Pakistan’s ongoing IMF programme is pushing toward removal of sector-specific tax incentives as part of fiscal consolidation. The 0.25% FTR for IT exports is precisely the kind of sector-specific concession the IMF flags as a tax expenditure.

There is a direct tension between:

- IMF position: Broaden the tax base, remove exemptions

- Pakistan IT sector position: Protect the exemption that created a $1 billion+ export base

The Finance Ministry must navigate both in the June 5 budget announcement.

Three Possible Outcomes — June 5, 2026

Outcome 1 — Extension as-is (Best case for freelancers)

The 0.25% FTR and Clause 133 exemption are both extended for at least one year. Status quo maintained. Probability: Moderate — industry lobbying has been strong.

Outcome 2 — Modified regime (Most likely)

The exemption is restructured — possibly:

- FTR extended but at a higher rate (e.g., 1% or 2%)

- Clause 133 exemption retained for individuals, FTR modified for corporate entities

- New documentation or registration requirements added

Outcome 3 — Exemption expires or is significantly curtailed

The 0.25% FTR is not renewed. Large IT exporters move to standard corporate tax. Individual freelancers retain Clause 133 exemption but face uncertainty. Probability: Lower after P@SHA retracted its proposal — but not zero given IMF pressure.

What Freelancers Need to Know Right Now

1. Your exemption requires proper remittance

Clause 133 exemption is conditional. If your foreign income is not coming through the banking channel (e.g., received in a foreign account and not repatriated), you do not qualify for the exemption. The income is taxable at normal rates.

2. The 80% rule is non-negotiable

At least 80% of export proceeds must be remitted to Pakistan through normal banking channels. The remaining 20% can be retained abroad.

3. You still have a filing obligation

Exempt income must still be declared in your income tax return (Section 116 wealth statement requirement). Undeclared foreign income is an increasing audit risk.

4. PSEB registration matters

If you are a company (not individual freelancer), PSEB registration is the gateway to the 0.25% FTR. Without it, standard rates apply to your export income.

5. The exemption does not cover domestic IT revenue

Clause 133 applies to export income only. If you earn from Pakistani clients, those earnings are taxable at standard slab rates (currently 1%, 11%, 23% per Finance Act 2025).

Current Tax Slabs — In Case the Exemption Disappears

If the IT exemption is removed or curtailed, individual freelancers earning from exports would be taxed under standard slab rates. For reference, Finance Act 2025 individual slabs:

| Annual Income | Tax Rate |

| Up to Rs. 600,000 | 0% |

| Rs. 600,001 to Rs. 1,200,000 | 1% |

| Rs. 1,200,001 to Rs. 2,200,000 | 11% |

| Above Rs. 2,200,000 | 23% |

Source: Division I, Part I, First Schedule — Finance Act 2025

Note: These are current rates. Budget 2026-27 may change these slabs as well — full analysis published June 5, 2026.

Read Also

- Salaried Class: Will You Finally Get Income Tax Relief in Budget 2026-27? — Tax-free threshold, surcharge removal, top rate cut.

- Property Investors: What Budget 2026-27 Could Change for You — CGT, withholding rates, FBR valuations.

Key Takeaways

- Clause 133 exemption: Currently in force — exempt from income tax if 80% remitted via banking

- 0.25% FTR for PSEB entities: Expires June 30, 2026 — must be renewed in Finance Act 2026-27

- P@SHA proposal: Retracted — but IMF pressure on exemptions remains

- PAFLA warning: $1 billion in freelance earnings at risk if rates increase

- Budget date: June 5, 2026 — full analysis published same day at clearconcept.academy

- All proposals are pre-budget as of June 3, 2026

Legal References

- Income Tax Ordinance 2001 — Clause 133, Part I, Second Schedule (IT exemption)

- Income Tax Ordinance 2001 — Section 113 (minimum tax on turnover)

- Income Tax Ordinance 2001 — Section 116 (wealth statement obligations)

- First Schedule, Part I, Division I — individual income tax slabs (Finance Act 2025)

- Finance Act 2025 — amendments to IT export incentives

- PAFLA statement, May 2026 — published via ProPakistani

- State Bank of Pakistan — freelancing remittance data July–April FY2025-26

All proposals are pre-budget expectations as of June 3, 2026. Nothing constitutes formal tax advice. Final changes confirmed in Finance Act 2026-27 following National Assembly passage.

Sir Usman FCCA

BSc (Hons) Applied Accounting — Oxford Brookes University

Registered Senior FBR Income Tax Practitioner

15 years C-level industry experience

ClearConcept Academy — Where Accountants Are Made

FIA · ACCA · Pakistan Taxation

clearconcept.academy | wa.me/923096755747

#Budget2026 #ITExemption #FreelancerTax #PakistanTax #FBR #PAFLA #PSHA #ITExport #PakistanBudget2627 #ClearConceptAcademy #TechExports #FreelancePakistan