Property Investors: What Budget 2026-27 Could Change for You

Date: June 2, 2026

Category: Pakistan Taxation · Budget 2026-27 · Pre-Budget Analysis

Status: Pre-budget proposals only — final rates confirmed June 5, 2026

Why Property Investors Need to Watch Budget 2026-27 Closely

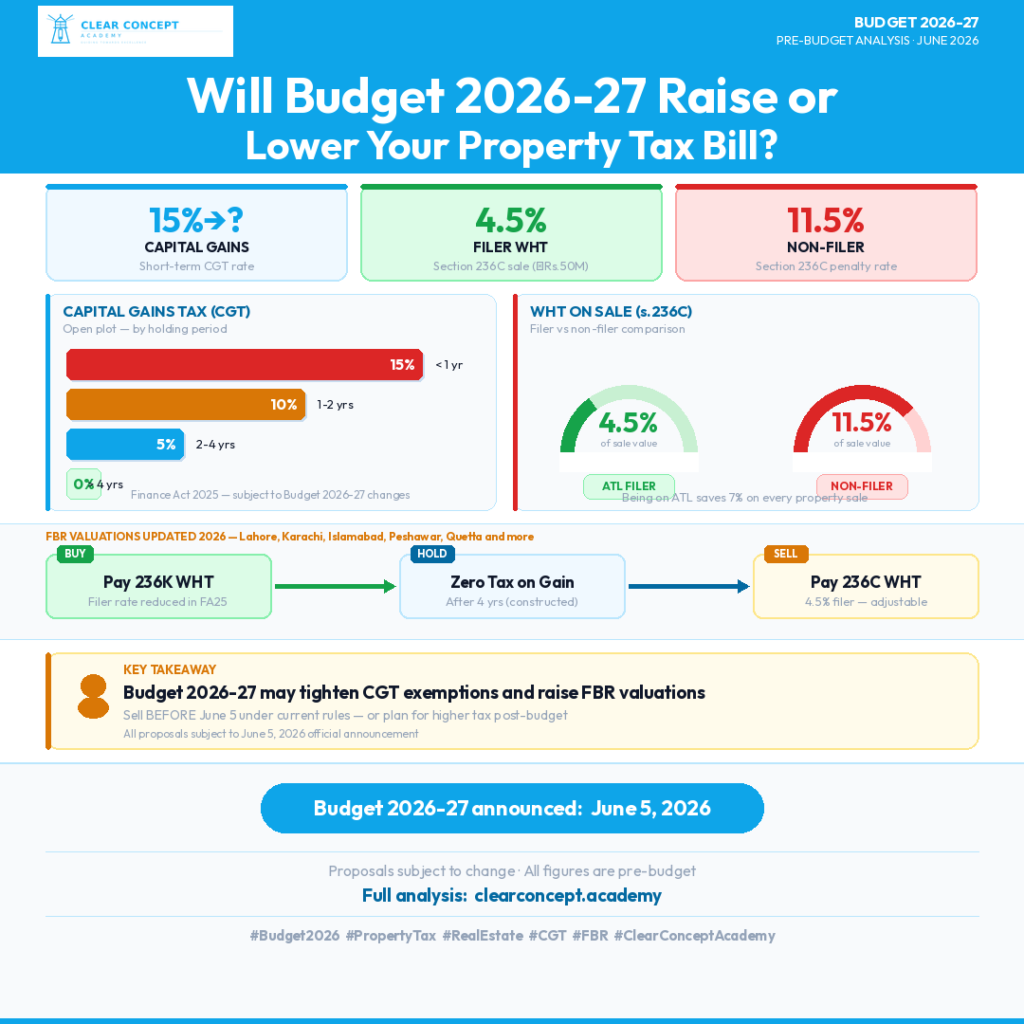

If you own property in Pakistan — whether you are a buyer, seller, developer, or long-term investor — Budget 2026-27 is not just noise. It has the potential to change the tax cost of every transaction you make.

The Federal Board of Revenue has already been tightening property taxation for three consecutive years. Finance Act 2023, Finance Act 2024, and Finance Act 2025 each introduced new measures targeting undisclosed property wealth, higher withholding rates for non-filers, and stricter FBR valuation tables.

Budget 2026-27, to be announced on June 5, is expected to continue this trajectory — with proposals targeting Capital Gains Tax, withholding rates, and FBR property valuations across all major cities.

Before the budget drops, here is exactly where things stand today — and what may change.

Where Things Stand Today — Finance Act 2025

Capital Gains Tax (CGT) on Immovable Property

For property acquired on or before June 30, 2024:

CGT is charged at slab rates ranging from 15% to 0% depending on the holding period.

| Property Type | Holding Period | CGT Rate |

|---|---|---|

| Open Plot | Up to 1 year | 15% |

| Open Plot | 1–2 years | 12.5% |

| Open Plot | 2–3 years | 10% |

| Open Plot | 3–4 years | 7.5% |

| Open Plot | 4–5 years | 5% |

| Open Plot | 5–6 years | 2.5% |

| Open Plot | Above 6 years | **0%** |

| Constructed Property | Up to 1 year | 15% |

| Constructed Property | 1–2 years | 10% |

| Constructed Property | 2–3 years | 7.5% |

| Constructed Property | 3–4 years | 5% |

| Constructed Property | Above 4 years | **0%** |

Source: Clause 104A, Part IV, Second Schedule, ITO 2001 — Finance Act 2025

Important: If your property qualifies for the 0% rate, you may apply for an exemption certificate under Section 159 — provided the property has been in personal use for 15 years, declared in wealth statement for 15 years, and appears as your residence in FBR records.

Withholding Tax on Sale — Section 236C

When you sell or transfer immovable property, the registrar collects advance tax at the time of registration.

| Seller Status | Consideration ≤ Rs.50M | Consideration > Rs.50M |

|---|---|---|

| ATL Filer | **4.5%** | **7.5%** |

| Non-filer / Late filer | **11.5%** | Higher rate |

Source: Division-X, Part IV, First Schedule — Finance Act 2025

Key change in Finance Act 2025: Seller rates were increased by 1.5% across all slabs — to be used as an adjustment against the capital gain on sale. This means if you are a filer selling property, the 4.5% collected is advance tax — adjustable in your annual return.

Withholding Tax on Purchase — Section 236K

When you buy immovable property, the registrar collects advance tax from the buyer.

- ATL filers: Rates were reduced by 1.5% in Finance Act 2025 (relief for compliant buyers)

- Non-filers: Significantly higher rates apply under the Tenth Schedule

Source: Division-XA, Part IV, First Schedule — Finance Act 2025

FBR Property Valuations — Updated 2026

FBR has issued new valuation tables for immovable property in all major cities:

- Lahore — Updated May 19, 2026

- Rawalpindi — Updated May 19, 2026

- Islamabad — Updated April 16, 2026

- Karachi — Amended (SRO 1724(I)/2024)

- Faisalabad — Updated April 21, 2026

- Gujranwala — Updated April 21, 2026

- Multan — Updated April 21, 2026

- Sialkot — Updated April 22, 2026

These valuations are critical — all withholding tax under S.236C and S.236K is calculated on the higher of the FBR valuation or the declared transaction value.

What Budget 2026-27 Could Change — Pre-Budget Proposals

These are proposals and expectations as of June 2, 2026. Nothing is confirmed until the Finance Bill is tabled on June 5.

Proposal 1 — Higher CGT Rates for Short-Term Flipping

FBR has signalled concern over speculative property transactions — particularly plot flipping within 1–2 years. A proposal under discussion would increase CGT rates on short-term disposals (under 2 years) to discourage speculation.

Likely impact: Investors who buy and sell within 1–2 years could face higher tax costs. Long-term holders (4+ years for constructed, 6+ years for plots) unaffected.

Proposal 2 — Further Tightening of Non-Filer Rates Under S.236C and S.236K

The Finance Act 2025 created a significant gap between filer and non-filer rates. Budget 2026-27 proposals include further increasing non-filer rates — making it substantially more expensive to transact property while outside the tax net.

Likely impact: Non-filers buying or selling property will face higher advance tax. Pressure to join ATL before transacting.

Proposal 3 — FBR Valuation Increase for Major Cities

FBR has updated valuations for most cities in early 2026. A further revision in the budget — bringing valuations closer to market value — is widely expected.

Likely impact: Higher declared transaction values means higher 236C/236K withholding on all transactions. Buyers and sellers both affected.

Proposal 4 — Deemed Income on Idle Property (Section 7E Extension)

Section 7E, introduced in Finance Act 2022, imposes a 20% tax on 5% of the FBR value of property not used for business or self-residence. An extension or tightening of this provision is under discussion.

Likely impact: Investors holding multiple properties as a store of value — without rental income — may face higher deemed income liability.

What Does Not Change — Regardless of Budget

Regardless of what Budget 2026-27 announces, the following remain:

- Filing deadline for Tax Year 2025: September 30, 2026

- Obligation to declare property in wealth statement: Section 116, ITO 2001

- FBR pre-loaded data: FBR already holds property registration records from registrars, NADRA, and land records authorities

- Advance tax is adjustable: All 236C and 236K collections are advance tax — adjustable in your annual income tax return if you are a filer

Three Things Property Investors Should Do Before June 5

1. Know your current CGT position.

If you are planning to sell property this year, calculate your CGT liability now under Finance Act 2025 rates. Know whether your holding period qualifies for a reduced or zero rate.

2. Ensure you are on the Active Taxpayer List (ATL).

The rate difference between filer and non-filer on property transactions is substantial — up to 7 percentage points on S.236C alone. Being off the ATL is expensive.

3. Declare all property in your wealth statement.

FBR property records are now integrated with land records, NADRA, and registrar data. Undeclared property is a growing audit risk — not a strategy.

Key Takeaways

- Current CGT: 15% → 0% based on holding period (Finance Act 2025)

- S.236C seller WHT (filer): 4.5% up to Rs.50M | 7.5% above Rs.50M

- FBR valuations: Updated for all major cities April–May 2026

- Budget date: June 5, 2026 — full analysis published same day at clearconcept.academy

- All figures in this article are current law (Finance Act 2025) + pre-budget proposals only

Legal References

- Income Tax Ordinance 2001 — Section 37 (Capital Gains), Section 236C, Section 236K, Section 7E, Section 116

- First Schedule, Part IV, Division X & Division XA — Withholding rates on immovable property

- Second Schedule, Part IV, Clause 104A — CGT exemptions and holding period table

- Finance Act 2025 — Amendments to 236C/236K rates

- FBR SROs (2026): Valuation tables for Lahore, Rawalpindi, Islamabad, Faisalabad, Gujranwala, Multan, Sialkot, Karachi

All proposals are pre-budget expectations as of June 2, 2026. Nothing constitutes formal tax advice. Final changes confirmed in Finance Act 2026-27 following National Assembly passage.

Sir Usman FCCA

BSc (Hons) Applied Accounting — Oxford Brookes University

Registered Senior FBR Income Tax Practitioner

15 years C-level industry experience

ClearConcept Academy — Where Accountants Are Made

FIA · ACCA · Pakistan Taxation

clearconcept.academy | wa.me/923096755747

#Budget2026 #PakistanTax #RealEstate #PropertyTax #FBR #CapitalGainsTax #PakistanBudget2627 #CGT #236C #236K #ClearConceptAcademy #PropertyInvestment #PakistanProperty

👉 Related Budget 2026-27 Analysis

Salaried Class: Will You Finally Get Income Tax Relief in Budget 2026-27? →

Tax-free threshold doubling, surcharge removal, top rate cut — complete pre-budget analysis.

👉 Also in This Series

Will Budget 2026-27 Kill or Protect the IT Exemption? →

0.25% FTR expires June 30 — Clause 133 rules, P@SHA controversy, PAFLA pushback, IMF pressure.